Credit Card Travel Rewards in the Philippines

New to travel rewards? This beginner-friendly guide explains how credit card travel points actually work in the Philippines.

Ate Len earns decent miles on her credit card. She knows this because the app tells her. She has no idea how many she needs for a flight, when they expire, or whether she should convert them to Mabuhay Miles or keep them as bank points.

Every few months she opens the rewards page, feels mildly confused, and closes it.

"Sana lang may nagpaliwanag sa akin ng simple," she once posted on r/PHCreditCards.

She got forty-seven replies. Most of them were optimized multi-card setups with spreadsheet templates.

That was not what she needed.

Ate Len is not a frequent flyer. She travels maybe once a year, sometimes less. She has a job, a family, and a full life that has no room for a second hobby called "points management." She just wants her card to quietly give her something useful without requiring a lot from her in return.

This article is written for Ate Len. And for everyone who nodded reading that.

👉 Credit Card Travel Rewards in the Philippines

The travel rewards content online is mostly written for a specific kind of person. The frequent flyer. The miles hacker. The person who genuinely enjoys comparing transfer partners, tracking bonus categories, and timing redemptions around award chart changes.

That person exists. They get a lot done with their points. But they are not most Filipinos.

Most Filipinos travel during the BER months or once a year for a family trip. They have fixed dates because of work and school schedules. They don't want to restructure their spending around a rewards calendar. And they find the idea of managing three cards for three different bonus categories mildly exhausting just to think about.

The problem is that complex systems don't just fail quietly for casual travelers. They fail loudly. People overspend chasing promos they half-understood. They make rushed redemptions just to feel like the system is working. They get frustrated and either give up entirely or keep a high-fee card they're not actually using well.

The complexity doesn't produce better outcomes for casual travelers. It just produces more stress.

👉 Beginner Mistakes Filipinos Make With Travel Rewards

Before getting into the steps, it helps to be clear on what you're aiming for.

A simple travel points system should require minimal effort to maintain. It should never change your spending behavior — you should be spending the same way you would without a rewards card, just on a card that gives something back. It should reduce regret, not create it. And it should feel optional. If the points come together into something useful, great. If a particular month or year they don't, that's fine too.

If your system fails any of those four things, it's too complex for your life. Simplify.

The whole system starts here. One card.

Not one for groceries and one for dining and one for travel. One card that you use for most of your regular spending — bills, groceries, online shopping, whatever your biggest categories are — and that earns points consistently across all of it.

The mental load of multiple cards is real. Different statement dates. Different reward structures. Different promos with different conditions. For a dedicated enthusiast who enjoys this, it's fine. For someone who just wants to quietly earn something while living their life, it adds anxiety without adding proportional value.

Pick the card that fits your spending best. Use it. Track one statement. That's it.

Cards like UnionBank Miles+, PNB Mabuhay Miles World, and BPI Platinum Rewards are examples that work as all-rounders for this approach — cards you can put most of your spending on without needing to optimize by category. But the specific card matters less than the principle: one main card, one rewards structure, one thing to think about.

👉 Should You Upgrade to a Travel Card — or Stick With Cashback?

If you're a casual traveler, flexible bank points are almost always better than airline-specific miles.

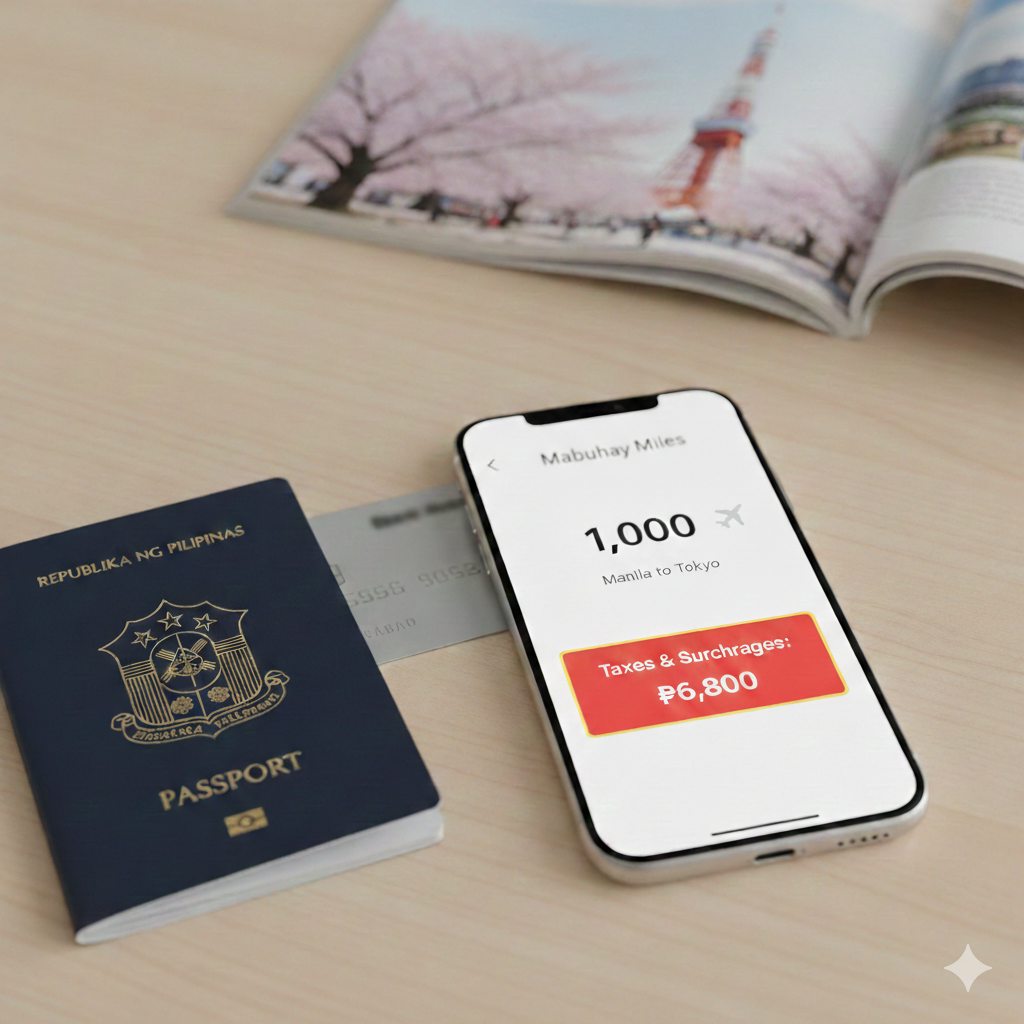

Here's why. Airline miles are optimized for one outcome: booking flights through that airline's award programme. When that works out — the right route, the right availability, the right timing — the value can be excellent. But getting there requires knowing the programme, monitoring availability, and often converting your bank points first.

Bank points are more forgiving. Many Philippine cards let you convert to multiple airline partners — Mabuhay Miles, GetGo, AirAsia BIG Points, KrisFlyer — which means you can decide later based on what trip you're actually planning. Some cards also let you use points for statement credits, hotel stays, or other redemptions if a flight doesn't work out.

For a casual traveler who doesn't know yet exactly where they're flying or when, keeping options open is more valuable than chasing the theoretically highest earn rate on one specific airline.

Optimization is for people who already know their target. Flexibility is for people who are still figuring it out.

👉 Airline Miles vs Bank Points: What's the Difference?

This step will save you more money than any promo ever will.

Card promos are designed to look like opportunities. Spend ₱30,000 this month and get 5,000 bonus miles. Use your card three times at this partner and earn double points. Hit this threshold by this date and unlock lounge access.

Some of these are genuinely useful — if the spend threshold matches what you were already going to spend anyway, and the reward is meaningful, and the timing works. That's a real win.

But most promos require you to do something you wouldn't otherwise do. Buy more than you need. Shift spending in ways that don't make financial sense. Rush a decision. And the value of the bonus, when you actually calculate it, rarely justifies the extra behavior it required.

The rule for casual travelers: if a promo fits naturally into your life without changing anything, use it. If it requires you to spend more, move faster, or add complexity — ignore it. The points you miss out on are almost never worth the friction you take on.

Not every points balance needs to be redeemed immediately. Not every opportunity is the right one.

Redeem when cash prices are high — peak season flights, popular destinations during holidays, long-haul routes where the savings are meaningful. Redeem when the fees and surcharges are reasonable relative to what you're saving. And redeem when the dates and routing already match your actual plans, not when you're forcing a trip around award availability.

If you're unsure whether a redemption makes sense, wait. Points sitting in your account are not wasted. They're waiting for the right moment. A mediocre redemption made out of impatience is worse than holding your balance for something genuinely useful later.

The casual traveler's advantage is that they're not trying to maximize every point. They're just looking for the moments where the discount is obvious and the process isn't painful. Those moments do come. You just have to not burn your points on a rice cooker before they arrive.

👉 How to Redeem Airline Miles Without Wasting Them

A good simple system doesn't force every decision through the points framework.

When Cebu Pacific has a seat sale with genuinely low fares, paying cash is probably smarter than burning miles. When you need a domestic flight next week and award availability is non-existent, just buy the ticket. When the lounge is overcrowded and the food is cup noodles, walking to Jollibee is a perfectly fine choice.

Choosing cash or cashback in these moments isn't a failure of your system. It's the system working correctly. A simple approach means using whatever tool makes the most sense in the moment — not defending miles as a lifestyle commitment regardless of circumstances.

Some months, points will do useful work. Other months, cash is just better. A simple system is relaxed enough to accept both.

👉 Cashback vs Miles: Which Is Better for Filipino Travelers?

Casual travelers do not need monthly optimisation sessions. They need one quiet check-in per year.

Pick a time that makes sense — maybe January, maybe before your usual travel season, maybe on your card anniversary. Spend twenty minutes on two things: check your points balance, and check when your points expire.

If you have a balance worth redeeming and a trip coming up that it makes sense for, start looking at availability. If you don't have a specific trip in mind, think about whether any activity before the expiry date can reset the clock on your balance. And if nothing makes sense yet, close the app and go back to your life.

That's the whole review. Twenty minutes. Once a year. No spreadsheet required.

Research on Filipino loyalty programme users shows that a lot of points expire unused not because people don't care, but because they never built in a moment to check. The annual review fixes that without turning rewards into a part-time job.

Put it all together and the system looks something like this.

You have one main rewards card that you use for your regular spending. You don't change what you buy or where you shop. You don't chase promos unless they happen to line up with something you were already doing. Once a year, you check your balance and expiry date. If there's a trip coming up and the math makes sense, you look into redeeming. If not, you wait.

That's it.

Points accumulate quietly in the background. Occasionally they turn into something useful — a cheaper flight, a meaningful discount on a trip you were going to take anyway. Most of the time they just sit there, not causing any problems, not requiring any attention.

You never feel pressure to "use them before they expire" because you're keeping an eye on expiry with your annual review. You never feel stressed about maximising because you're not trying to maximise. You just want something back for spending you were already doing.

That's not a consolation prize version of travel rewards. That's actually the right version for most people.

If any of these sound familiar, it might be time to simplify:

None of these are signs that you're bad at travel rewards. They're signs that the system has grown beyond what you actually want from it. Complexity crept in slowly and it's now doing more harm than good.

The fix is always the same: go back to one card, one annual check-in, redeem only when it's obviously worth it. Let the rest go.

The best travel points system is not the one that extracts maximum value from every peso you spend.

It's the one you'll still be using five years from now without feeling burned out by it.

Ate Len eventually simplified. She dropped one of the two cards she'd been half-managing, started using a single rewards card for her main spending, and set a reminder to check her balance every January. Last year she used her points toward a Bohol trip during long weekend. Not a maximised redemption by any measure. But she knew what she had, she used it at a moment that made sense, and she didn't have to think about it too hard.

"Mas okay na," she said. "Di na ko stressed."

That's what a good system feels like.