How Credit Card Travel Points Actually Work in the Philippines

Confused about travel points? This beginner-friendly guide explains how credit card travel points actually work in the Philippines — without hype or shortcuts.

Learn From Other People's Expensive Mistakes

One advantage of Reddit is brutal honesty.

Filipinos openly share:

Last week, someone posted on r/PHCreditCards:

"I got a travel card two years ago. Annual fee: ₱5,000. I earned 18,000 miles. I never redeemed them. They expired last month. I'm an idiot."

The replies weren't harsh. They were understanding.

"Same thing happened to me."

"I did this with three different cards."

"At least you're not alone."

This article compiles the most common travel rewards mistakes beginners make — based on real discussions, not theory.

Many users admit:

"I applied because it looked premium."

r/PHCreditCards is full of posts where people signed up for "premium" or travel cards because they looked aspirational, then later realized the rewards didn't fit their actual lifestyle or spend.

Example from Reddit (paraphrased):

"I got the Citi PremierMiles card kasi mukhang sosyal. Annual fee ₱3,800. After one year, I realized I don't travel enough to justify it. I asked for a waiver. They said no. I canceled it. Sayang."

Travel cards aren't lifestyle upgrades. They're financial tools.

Skipping the learning phase leads to regret.

What happens:

Threads show users applying for cards like Citi PremierMiles or bank travel signatures, then only later asking whether the annual fee is worth it or what to do when waiver requests fail.

How to avoid it:

Before applying for any travel card, ask yourself:

If you answered "no" to any of these, don't apply yet.

Believing: "Miles = money"

Leads to:

Multiple PH Reddit posts explicitly ask what air miles are worth in pesos and complain that bank points-to-miles conversions and redemptions feel like a "rip-off" once they do the math.

Example from Reddit (paraphrased):

"I have 25,000 BPI points. I thought that's ₱25,000. I tried to convert to PAL miles. I only got 5,000 miles. I checked how much those miles are worth. Maybe ₱4,000 in flight value. Ang laki ng nawala."

Users describe how converting to PAL Mabuhay Miles or taking shopping credits yields much less value than they expected, showing the danger of treating miles as "money" instead of a conditional discount.

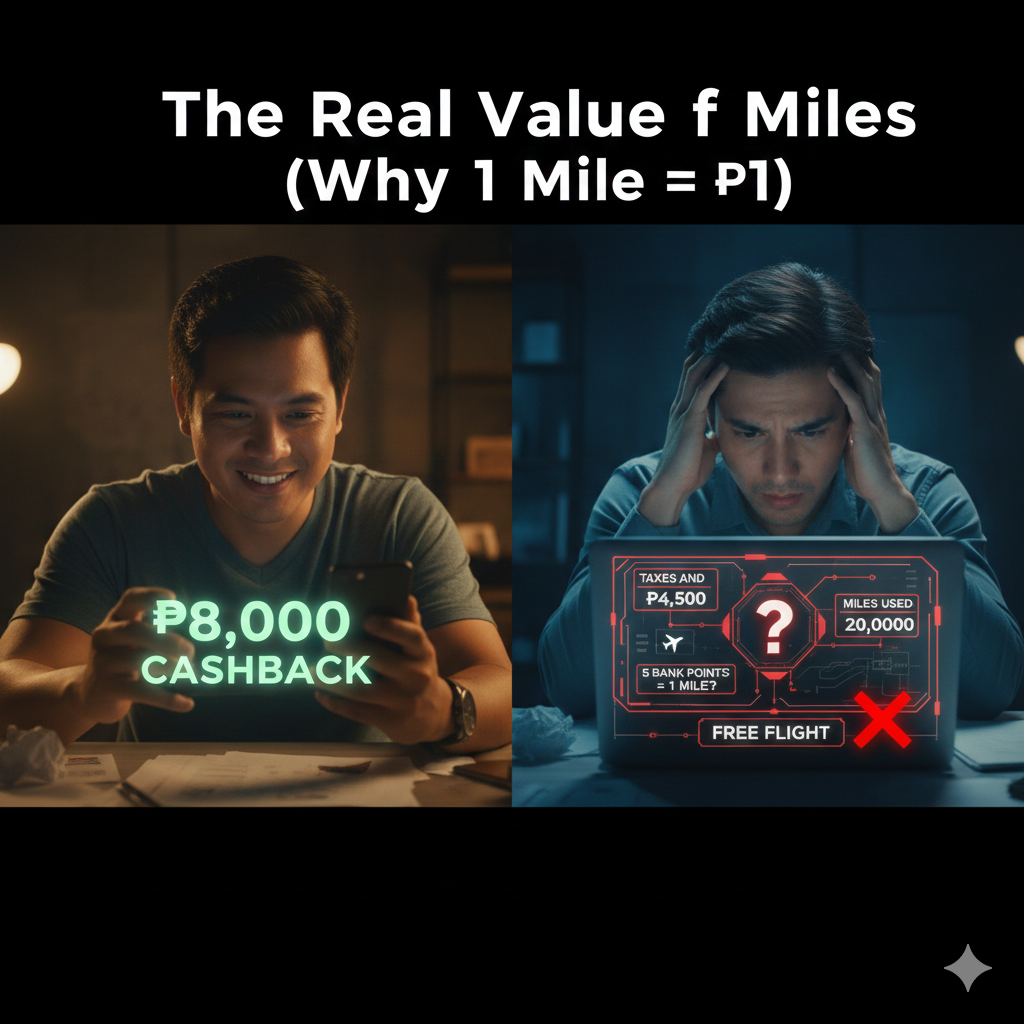

Reality check:

1 mile ≠ ₱1.

Usually, 1 mile = ₱0.40–₱0.80 in redemption value. Sometimes less.

Real story:

Mark had 50,000 miles. He assumed that's ₱50,000 worth of flights.

He tried to book Manila–Singapore. The system wanted 30,000 miles + ₱6,500 in taxes.

The same flight on a promo fare? ₱12,000.

He saved ₱5,500 using 30,000 miles.

That's ₱0.18 per mile.

Not ₱1.

Hitting spend thresholds early feels productive — but often leads to unnecessary purchases.

Points-and-miles discussions (PH and global) show many cases of people spending extra to hit sign-up bonuses or promo thresholds, then realizing the incremental spending outweighed the rewards benefit.

Example from Reddit (paraphrased):

"My card had a promo: spend ₱80,000 in 3 months, get 10,000 bonus miles. I hit it in 2 months. Looking back, I bought a lot of things I didn't need just to reach the threshold. The bonus miles are worth maybe ₱8,000. But I spent at least ₱20,000 extra. Tanga."

What happens:

A PH miles thread highlights that big redemptions (like business class to Europe) came from very high, consistent monthly spend (₱300k–₱700k), not from forcing purchases just "for points."

How to avoid it:

Ask yourself before every purchase:

"Would I buy this if there was no bonus?"

If the answer is no, don't buy it.

Many users admit:

"I forgot about the annual fee."

r/PHCreditCards has posts where users only notice or question the annual fee at renewal, then scramble to ask if they can cancel to avoid it or negotiate waivers after the charge appears.

Example from Reddit (paraphrased):

"My card just charged me ₱4,500 annual fee. I didn't use the card much this year. Can I get it waived? Or should I just cancel?"

Annual fees change the math completely.

Reality:

That's not bad. But only if you actually redeem.

If you don't redeem? You paid ₱4,500 for nothing.

How to avoid it:

Before signing up, calculate:

"How much do I need to spend — and redeem — to beat the annual fee?"

If the answer feels unrealistic, choose a different card.

Some users report success in getting waivers after threatening cancellation, while others note that high spend doesn't always guarantee a waiver. Annual fees are a real, recurring cost, not a footnote.

Points often expire because:

Expired points have zero value.

Example from Reddit (paraphrased):

"I had 22,000 BPI points. I was waiting to accumulate more before converting to PAL miles. Then I got a text: 'Your points will expire in 30 days.' I tried to convert. Minimum conversion is 5,000 points = 1,000 miles. I converted 20,000 points to 4,000 miles. Then BPI changed their conversion rate. My remaining 2,000 points became useless. They expired."

While not always framed as "I let them expire," PH users complain about sitting on points for years, only to confront devaluations, poor conversion options, or impending expiry notices.

Bank rewards FAQs and user rants both highlight that bank programs reserve the right to change rates or terms, effectively punishing those who hoard instead of redeeming thoughtfully.

What happens:

How to avoid it:

Set calendar reminders for:

Or better yet: redeem regularly instead of hoarding.

Bad redemptions are common when:

Patience matters.

People frequently post after redeeming for weak options like low-value gift certificates or travel credits, then realizing they could have gotten more value with a different strategy or even with simple cashback.

Example from Reddit (paraphrased):

"My points were about to expire. I couldn't find any good flight redemptions. I converted to shopping vouchers instead. ₱5,000 worth of vouchers for 25,000 points. Later I realized if I waited a bit and redeemed for a flight, I could've gotten ₱12,000 worth of value. But I panicked."

Some PH users explicitly say they feel forced to "use up" points before devaluation or card cancellation, leading to suboptimal redemptions that create regret.

What happens:

How to avoid it:

Plan redemptions before you're under pressure.

If you can't redeem well, sometimes it's better to let points expire than to redeem poorly.

At least you won't feel the sting of "I wasted 50,000 points on ₱3,000 worth of stuff."

Interest wipes out rewards faster than people expect.

Credit education pieces aimed at Filipinos stress that interest and charges quickly overshadow reward value and identify minimum-payment habits as a core danger.

Example from Reddit (paraphrased):

"I paid the minimum for 6 months kasi tight ang budget. I earned 4,000 miles during that time. But I also paid ₱8,500 in interest. The miles are worth maybe ₱3,200. I lost ₱5,300. Never again."

In points forums, seasoned users repeatedly remind others that paying interest "kills" the value of miles or cashback.

The math:

Next month:

After 6 months of paying minimum, you could pay ₱5,000–₱10,000 in interest.

The miles you earned? Maybe ₱2,000–₱4,000 in value.

You lost money.

How to avoid it:

Pay in full. Every month. No exceptions.

If you can't pay in full, you're spending too much.

Simple habits:

Advice like "pay in full," "treat points as optional," and "would I buy this without rewards?" lines up with best practices recommended by financial literacy resources and card behavior articles.

Real advice from a Reddit user (paraphrased):

"Treat your travel card like a debit card. If you don't have the cash to pay the full statement, don't use the card. Rewards are a bonus, not a reason to spend."

Travel rewards should:

If they don't, something is wrong.

Positioning travel rewards as something that should reduce stress and feel optional, not like a milestone or status symbol, aligns with recurring PH posts where people end up canceling "premium" cards that turned out to be more hassle than help.

Example:

After two years of stressing over points, conversions, and redemptions, Ana canceled her travel card.

Her friends asked: "Bakit? Sayang naman yung rewards."

She said: "Mas sayang yung peace of mind ko."

She switched to cashback. Simple. Predictable. Walang stress.

She still travels. She just pays with cash now. And she's happier.

Learning from others is cheaper.

Every mistake in this article cost someone real money. Some lost hundreds. Some lost thousands.

You don't have to repeat their mistakes.

Last thought from Reddit (paraphrased):

"I wish someone told me: travel cards aren't for everyone. They're for people who travel a lot, spend a lot, and enjoy planning. If you're not that person, cashback is better. I learned this the expensive way. You don't have to."

Use their regrets wisely.