Savings Account vs Time Deposit: What's Better for Filipinos?

The real differences for Filipinos — and how to choose based on flexibility, goals, and peace of mind.

"Mag-digital bank na ba ako?"

This question is everywhere.

Sa Facebook groups, Reddit, TikTok comments — lagi may nagtatanong. "Yung digital bank kasi, mas mataas ang interest. Should I move all my savings na?"

And honestly? The excitement makes sense.

When you see a digital bank advertising 6% or even 10% interest, and your current bank is giving you 0.25%, parang obvious na ang sagot.

But rate differences are only one part of the story.

The better question isn't "which bank pays more?" It's "which setup actually works for how I live?"

This guide walks through the real trade-offs — so you can choose based on your situation, not just a headline number.

If you're still figuring out the basics of where to put your money, start here first: 👉 Savings Account vs Time Deposit: What's Better for Filipinos?

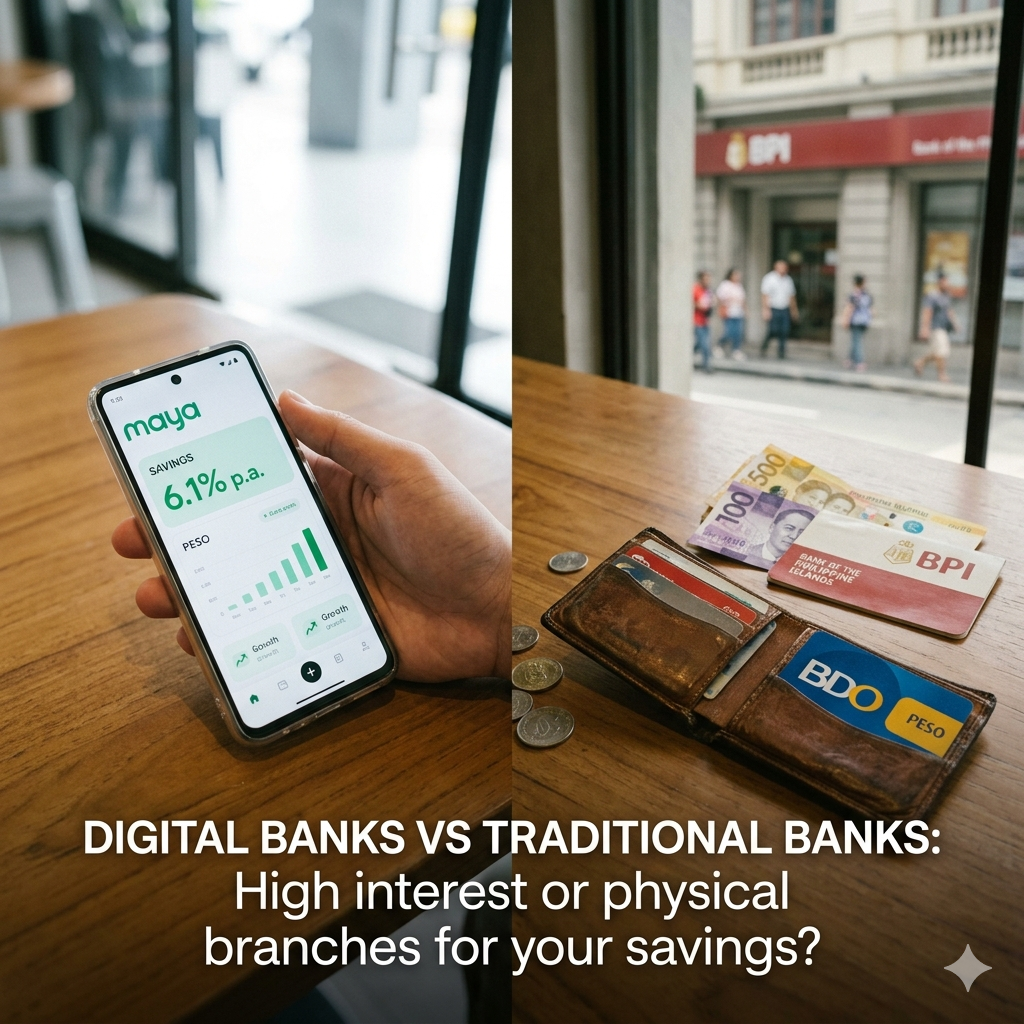

It's not just the rates. Although, yes — the rates are significantly higher.

Philippine digital banks advertise savings accounts with base rates around 3–4% per year. Some even promote rates of 10–15%, though those come with conditions we'll get into shortly.

Compare that to many traditional savings accounts, which still sit well below 1% per year.

Beyond the numbers, digital banks just feel easier.

Account opening takes minutes. Walang pila. Walang forms na pipirmahin. Hindi ka na kailangang mag-leave para pumunta ng branch. Your balance updates in real time, and some banks credit interest daily — which sounds small, but it's genuinely motivating when you're trying to build a habit.

Many also let you start with as little as ₱250 to ₱1,000. That matters for students, fresh grads, and gig workers who aren't working with big amounts yet.

Situation: Renz is a 24-year-old freelance video editor. Irregular ang income niya, so hindi siya nag-aral ng masyado sa savings noon. Nung nakita niya na puwede siyang mag-open ng digital savings account in five minutes — no maintaining balance, earning 4% interest — nag-start na siya mag-ipon for the first time. Hindi siya convinced ng rates. Convinced siya ng dali.

Traditional banks aren't going anywhere. And for good reason.

Their biggest advantage is physical access. Universal and commercial banks have branches and ATMs across the country — kahit sa probinsya, kahit mahina ang signal, kahit patay na ang phone mo.

They're also deeply wired into how money actually moves in the Philippines. Payroll, remittances, government payments, and most big business transactions still go through traditional banks. Para sa marami, hindi ganoon kadali ang "mag-switch" — especially kung doon din napupunta ang sweldo mo.

And when something goes wrong — a disputed transaction, a missing transfer, a fraudulent charge — some people strongly prefer sitting across from a real person who can pull up the account and fix it on the spot. Hindi lahat comfortable sa in-app chat pag nasa problema na.

Situation: Ate Marie, 52 anos, nanggaling sa Batangas papuntang Manila para mag-withdraw ng malaking halaga para sa kasal ng anak niya. Hindi siya familiar sa digital transfers. Para sa kanya, mas ligtas na makita niya mismo ang transaction — makausap ang teller, makuha ang slip. Trabaho ng traditional bank ang ganitong peace of mind.

Situation: Lolo Ben is 68. His pension is deposited into a traditional bank. His daughter once tried to set up a digital bank account for him para mas mataas ang interest. Three attempts at the selfie verification later, binitawan na nila. The branch is five minutes from their house. Yun na ang pinaka-logical na choice.

Let's be honest about the numbers.

Base savings rates at most Philippine digital banks: around 3–4% per year. Already meaningfully higher than sub-1% traditional savings.

But the promo rates — the "up to 10–15%" in the ads — come with conditions:

And even when you qualify, the higher rate usually applies only to a capped balance — say, the first ₱100,000 to ₱250,000. Everything above that earns the lower base rate.

Situation: Gab signed up for a digital bank because of the advertised 10% rate. Pero hindi niya na-meet ang monthly spend requirement nung isang buwan kasi mag-ipon siya, hindi maggastos. Yung month na yun, earned siya ng 4% lang — na okaya pa rin, but not what he expected.

The honest math: On ₱100,000 for one year, the difference between 0.5% and 4% is roughly ₱3,500. Helpful — pero hindi life-changing. On ₱500,000, that same gap becomes ₱17,500 a year. Yun na ang time na talagang sulit pag-usapan ang rates.

Marami ang may maling akala dito.

Both digital banks and traditional banks that are licensed by the Bangko Sentral ng Pilipinas (BSP) are required to be PDIC members — Philippine Deposit Insurance Corporation. Hindi optional yun. Requirement siya para makapag-operate.

As of 2025, PDIC insures deposits up to ₱1,000,000 per depositor, per bank, covering both principal and earned interest. Savings accounts, checking accounts, time deposits — kasama lahat, in peso and eligible foreign currency.

Ang ibig sabihin: a PDIC-insured digital bank and a PDIC-insured traditional bank offer the exact same deposit protection. The brand name or the physical building doesn't change the coverage.

Situation: Jess had ₱800,000 in a traditional bank and was worried about moving ₱400,000 to a digital bank. Pagkatapos niyang basahin ang PDIC coverage, narealize niya na under ₱1M pa rin ang bawat account — both fully insured. Hindi siya nag-aatubili pa.

The more important question comes when you go above ₱1 million.

If you have more than ₱1M in a single bank — digital or traditional — the excess sits outside PDIC coverage. Ang solusyon: spread your funds across two or more BSP-licensed banks para mas malaki ang portion na insured.

Digital banks work well in specific situations.

Situation: Tin is saving for a trip to Japan in eight months. Inilagay niya ang ₱5,000 monthly sa isang digital savings account na may 4% interest. Di niya hahawakan kasi labeled siya as "Japan 2026." Yung visual separation alone ang nakatulong na hindi niya gamitin.

Situation: A freelance graphic designer with irregular income keeps a traditional bank account for client payments and monthly bills. Every payday, she manually transfers her "savings" portion to a digital bank — a different app, a different account number. Yung extra step na iyon ang nagsilbing barrier para hindi niya ma-access nang basta-basta.

These are usually high-pressure situations. And that's exactly when bank access matters most.

Situation: Nico kept his emergency fund at a digital bank for higher interest. Nung nagkasakit ang nanay niya at kailangan ng pera for hospital admission, na-delay siya ng halos isang araw dahil sa transfer limit ng app at cut-off time. Hindi naman malaking abala — pero hindi rin yung timing na gusto mong mag-abala.

Situation: Carlo and his wife were buying a condo unit. The developer required a manager's check for the reservation fee. Ang alam niya sa digital banking, hindi siya agad makakagawa ng ganon. Kailangan pa rin niya ang traditional bank for that transaction.

Hindi kailangan pumili ng isa.

The setup na gumagana para sa karamihan: parehong gagamitin, iba-iba ang purpose.

Situation: Mia is a 29-year-old HR officer. Ang setup niya: three months of expenses sa traditional bank (malapit sa opisina ang branch). The next six months of buffer nasa GoTyme higher interest, but she still has InstaPay access if needed. Yung extra savings niya for her apartment deposit? Time deposit sa isa pang digital bank, earning 5.5% for 12 months. Hindi niya hahawakan yun.

Situation: An OFW family routes remittances through a traditional bank linked to their beneficiary's ATM card. Pero yung mga natitipid na hindi kailangan ngayon? Napupunta sa digital savings account ng nanay, na-set up ng anak bago umalis, mas mataas ang interest, at kaya pa ring i-access kapag emergency.

👉 When a Time Deposit Makes Sense (And When It Doesn't)

Ito yung parte na hindi masyadong pinag-uusapan.

Digital bank rates change. Promos expire. New ones launch. And because the Philippine personal finance community — lalo na sa social media — tracks these updates closely, may culture na ng "mag-jump sa pinaka-mataas na rate ngayon."

Pero yung constant movement ay may cost.

Bawat transfer ay may limits, cut-off times, and sometimes temporary holds on large amounts. Bawat move is another chance to send to the wrong account, miss a payment date, or accidentally spend what was supposed to be untouchable.

Meron din ang mental fatigue. Monitoring three to five apps, chasing promo requirements, setting reminders to move funds before a promo expires — this adds stress to your life. Ang savings ay dapat mag-reduce ng financial anxiety. Hindi dagdag sa anxiety.

Situation: Iya spent three months hopping between digital banks chasing the best promo rates. On paper, she was earning "up to 12%." Sa katotohanan, dalawang beses siyang nag-miss ng requirement, isang beses na-delay ang transfer, at minsan na nagamit ang pera dahil nasa "wrong account" na hindi niya obvious na iyon ang savings niya. Pag kinompute niya, kumita siya ng halos 4% lang for the year — pero mas stressed siya kaysa noon.

The more you treat savings like a game of musical chairs, mas madali mong maabot ang pera na dapat sana ay hindi mo hinahawakan.

Isang slightly lower rate na consistently maintained will almost always beat a theoretically higher rate that you keep disrupting.

Skip the comparison charts muna. Tanungin mo ang sarili mo:

Three more situations:

Wala sa tatlong ito ang mali. Built around the same core question: what does this money need to do, and when might I need it?

A 3% difference in interest matters. Pero mas hindi ito mahalaga kung ang paghabol mo rito ay nagdudulot ng stress, pag-iisip nang sobra, o paggamit ng pera na hindi mo dapat gagalawin.

The best savings setup isn't the one with the highest advertised rate.

It's the one that works when things aren't going according to plan.

Piliin ang setup na makakatulog ka sa gabi.