How Often Should You Review Your Savings?

Monthly, quarterly, or never? How often to look at savings without spiraling.

Marga checks her savings account almost every day.

Not because something is wrong. Not because she's planning a transfer. Just because. She opens the app, looks at the number, closes it. Sometimes she opens it again an hour later. She's not sure what she's looking for. But not checking feels worse than checking.

Her officemate Dara hasn't looked at her savings account in eight months. She set up an auto-transfer when she got her first job and hasn't touched the setup since. She tells herself it's because she trusts the system. But honestly? She's just been avoiding it.

Neither approach is working. Marga is exhausted. Dara is in the dark.

Personal finance creators like Your Rich BFF, Vivian Tu, make a similar point in different words: your savings need tending, not babysitting. Constant monitoring doesn't automatically build wealth, but total avoidance doesn't either. What actually works is a simple, regular check-in that gives you the information you need and then lets you move on.

This article walks through exactly what that looks like.

If reviewing your savings already feels stressful before you even start, read this first: 👉 How Often Should You Review Your Savings?

Monthly reviews sound responsible. In practice, they're often just an invitation to spiral.

Month-to-month, balances fluctuate for reasons that have nothing to do with your long-term habits. One month you saved more than usual. The next, a birthday or a long weekend wiped it out. A promo rate quietly dropped. None of that is meaningful data by itself. But if you're checking every four weeks, your brain treats every wiggle like a crisis.

Filipino money coaches such as Chinkee Tan have said this in many ways: the problem usually isn't that people don't know how to save, it's that emotions end up driving the financial decisions. Frequent checking can feed that cycle. Every dip feels like failure. Every uptick feels like permission to spend.

Quarterly reviews match how savings actually behave. Enough time passes that real changes become visible. Income shifts show up. Spending patterns reveal themselves. Progress actually registers.

In surveys by the Bangko Sentral ng Pilipinas, emergencies are the single most common reason Filipinos say they save at all, more than goals like retirement or travel. For that kind of security-focused saving, micromanagement isn't the goal; protection and consistency are. A quarterly rhythm gives your savings room to work.

Often enough to catch drift. Not often enough to become a hobby.

Open your accounts. That's it.

Note what's in your emergency fund. Note what's in your longer-term savings bucket. Don't analyze yet. Don't compare to last quarter. Don't calculate percentages. Just observe.

This step exists because avoidance is the more common problem. A recent study reported that only around 2 in 10 Filipinos have emergency funds that could cover more than three months of expenses, which means most households are still vulnerable to even medium-sized shocks. Thin buffers are not just about low income; they also grow quietly weaker when people stop looking, stop tracking, and let the account flatline.

Personal finance educators sometimes call this the "financial ostrich" move: head in the sand feels safer in the moment, but the number doesn't improve just because you stopped looking. Opening the app and seeing clearly what's there is already doing something real. It breaks the avoidance loop before it hardens into a pattern.

Even if the number is smaller than you'd like, you're ahead of where you'd be if you never looked.

👉 Small Savings Are Not Pointless (Despite What Social Media Says)

Don't run calculations. Don't assess your savings rate against a benchmark. Just ask yourself one thing:

If an unexpected expense hit this week, would it still be manageable?

That's the question. That's the whole review.

This matters because research shows that about 70% of Filipino families put financial preparedness for health emergencies at the top of their money concerns. Not retirement projections. Not maximizing investment returns. Just: what happens if someone gets sick?

Your savings buffer exists to answer that question. The quarterly check-up is just confirming it still can.

Filipino personal finance advocates like Aya Laraya often emphasize this: the purpose of an emergency fund isn't to make you rich. It's to make bad days survivable. If your savings can absorb a surprise without you having to borrow or panic, they're doing exactly what they're supposed to do.

If the answer to the stability question is yes, move on. If it makes you genuinely nervous, something small needs adjusting. The next steps handle that.

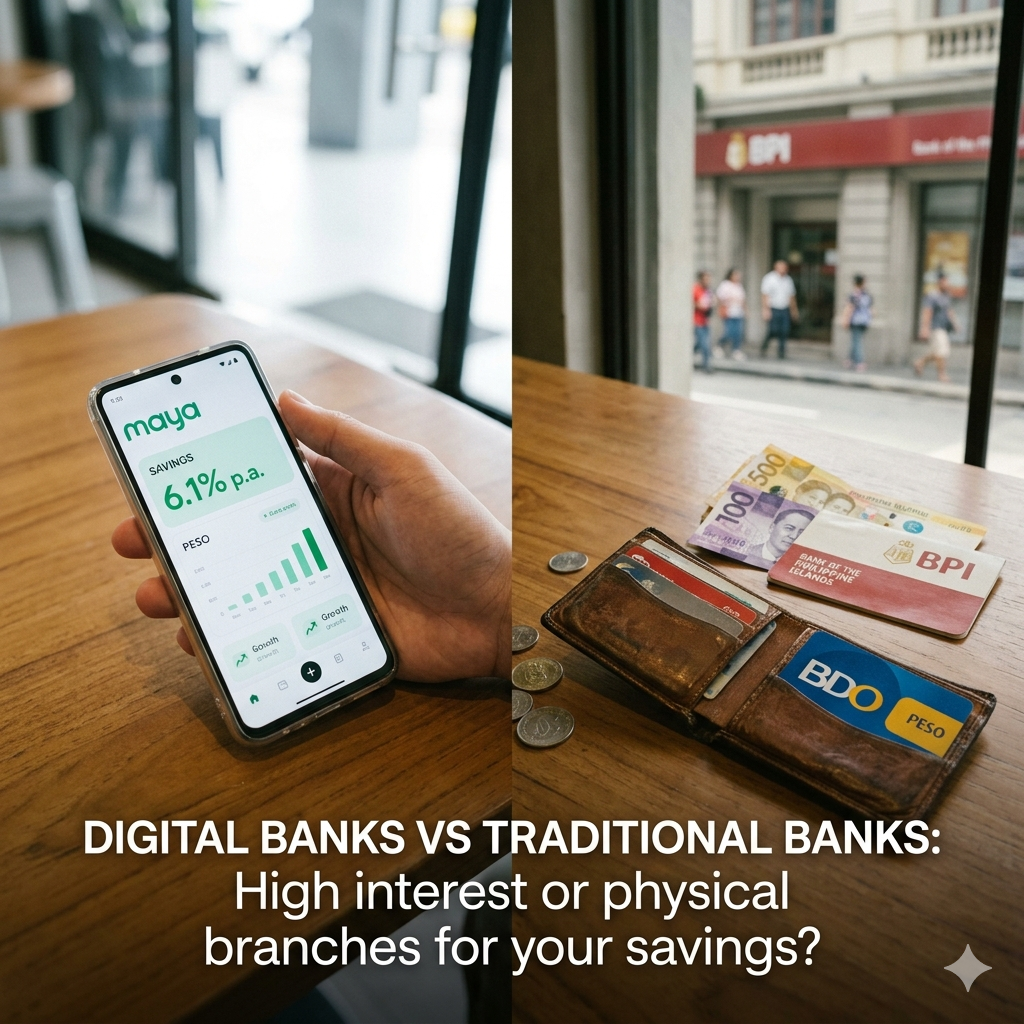

Interest rates get all the attention. But access is what actually matters when money is needed fast.

Check whether transfers are still smooth. Check whether any new fees appeared on your account. Check whether a promo rate quietly dropped — many digital savings products launch with high teaser rates and then adjust them downward later, so if you chose an account specifically for its rate, it's worth knowing if the conditions changed.

This step is practical, not obsessive. You're not optimizing. You're making sure the plumbing still works.

As creators like Vivian Tu often remind their audiences, a slightly higher interest rate means nothing if you can't actually get to your money when you need it. Reliability beats yield for emergency savings. A savings account you can access clearly and quickly in a stressful moment is worth more than one that technically pays more but comes with conditions you barely remember.

👉 Digital Banks vs Traditional Banks for Savings

If your income or expenses changed significantly in the last three months, this is the moment to reflect that in your savings setup.

Got a raise? Consider nudging your monthly contribution slightly higher. Moved somewhere more expensive? Your savings rate might need to flex down temporarily while you stabilize. Had a quarter where an unexpected expense hit the buffer harder than usual? A small increase to the auto-transfer for the next few months can help rebuild it.

The keyword is lightly. Coaches like Chinkee Tan come back to this again and again: sustainable habits beat intense, short-lived commitments. Going from saving nothing to saving 30% of your income in one month almost never sticks. The motivation collapses after the first tough week, and you're back to zero.

BSP survey data shows that among Filipino households who are able to save, about one-third say they aim to put away at least 10% of their monthly income, while the rest save a smaller share. The ones who actually sustain that 10%-ish level tend to build toward it gradually — small, durable adjustments that survive a bad month instead of dramatic pledges that don't.

👉 A Simple Savings System for Young Professionals

This step is just as important as anything else on the list.

Ignore month-to-month balance changes. One good month and one rough month don't tell you anything meaningful about your long-term savings health.

Ignore normal promo rate movements. Digital savings products adjust their rates regularly. If your app was showing a higher rate and now it's showing a lower one, that's worth noting in Step 3 — but it's not, by itself, a reason to blow up your whole approach.

Ignore social benchmarks. "By 30, you should have X saved." "People your age have Y in their accounts." These figures don't know your income, your family obligations, how much you send home, or what city you live in. They're noise dressed up as data.

Personal finance creators, including Your Rich BFF, often warn that constant comparison is the fastest way to feel broke even when you're not. Someone else's savings number reflects their income, their expenses, their life — none of which is yours. The only benchmark that really matters is whether your savings are moving in the right direction for your situation.

👉 How Much Savings Should You Actually Have in Your 20s and 30s?

Intentional filtering protects your consistency. Every time you choose not to react to something that doesn't actually matter, you protect the habit.

You've checked the balances. You've asked the stability question. You've reviewed access. You've made one small adjustment if needed. You've decided what to ignore.

Now close the app.

Don't tinker. Don't move money around just because you suddenly feel like optimizing. Don't open a new account because a promo caught your eye. Don't start calculating what you'd have in five years if you just switched to a slightly higher rate.

Investment educators like Marvin Germo often point out that investors who check their portfolios obsessively tend to make more emotional trades and can end up worse off than long-term investors who review periodically. The same logic applies to savings. Constant monitoring doesn't automatically improve outcomes. It more often increases anxiety and triggers impulsive moves — chasing promos, making transfers that feel productive but aren't, or loosening the budget after a good month because the balance looked "healthy enough."

The check-up ends when you close the app. Not when you've solved everything. Review, decide one small thing if anything needs adjusting, then move on with your day.

Quarterly is the rhythm for normal conditions. But life doesn't always stay normal.

An extra check-up makes sense when income suddenly changes, whether that's a new job, a lost project, or a cut in hours. It makes sense after a major expense that hit the buffer harder than expected. It makes sense when financial anxiety spikes and you've been avoiding the app for weeks.

Even then, the same six steps apply. You don't need a new, more complicated process for stressful moments. You need the same simple process, repeated calmly.

The structure exists precisely for moments when it's tempting to either panic or avoid. It gives you something specific and manageable to do instead of either extreme.

The goal was never just a number. The goal was to feel less reactive.

A healthy savings habit looks like less panic when something unexpected comes up. It looks like faster recovery after a rough month. It looks like not immediately reaching for utang the moment something breaks. It looks like making deliberate choices instead of desperate ones.

These are behavioral signs, not numerical ones. They don't show up on an app. But they're real, and they matter more than whatever rate your account is currently paying.

Advisers like Aya Laraya often point out that the clearest sign your financial life is improving isn't just a bigger balance. It's fewer moments of genuine panic. Fewer reactive decisions. More capacity to absorb what life throws at you without everything immediately becoming a crisis.

That's what savings are for.

If your savings review feels like a performance evaluation, you're doing too much.

Four times a year, six steps and no spreadsheets. No guilt about where you are relative to someone else's financial highlight reel.

Open the app. Check the balances. Ask one question. Review access. Make one small adjustment if needed. Decide what to ignore. Close the app.

The best system isn't the most sophisticated one. It's the one that lets you check in, make a small correction if necessary, and then get back to your life.

Yun lang ang kailangan. Move on with your day.