Are High-Interest Savings Accounts Too Good to Be True?

How to evaluate high rates without falling for hype — conditions, caps, and effective vs advertised rate.

Every month, someone posts an update online.

"Bank A raised their rate to 7%." "Bank B just dropped theirs." "May better option na daw sa Bank C."

And you feel it. That small pull. The sense that you're leaving money on the table by staying where you are.

So you move. At first, it feels responsible. Like you're being smart with your money.

But six months later, you realize you've opened four accounts, split your savings across three apps, and you still don't feel like you're getting ahead.

That feeling has a name. It's not financial discipline.

It's optimization fatigue.

This article is about breaking out of that loop and finding a savings setup you can actually stick with.

If you're still figuring out the basics of where savings should go, start here: 👉 Savings Account vs Time Deposit: What's Better for Filipinos?

It makes sense on the surface.

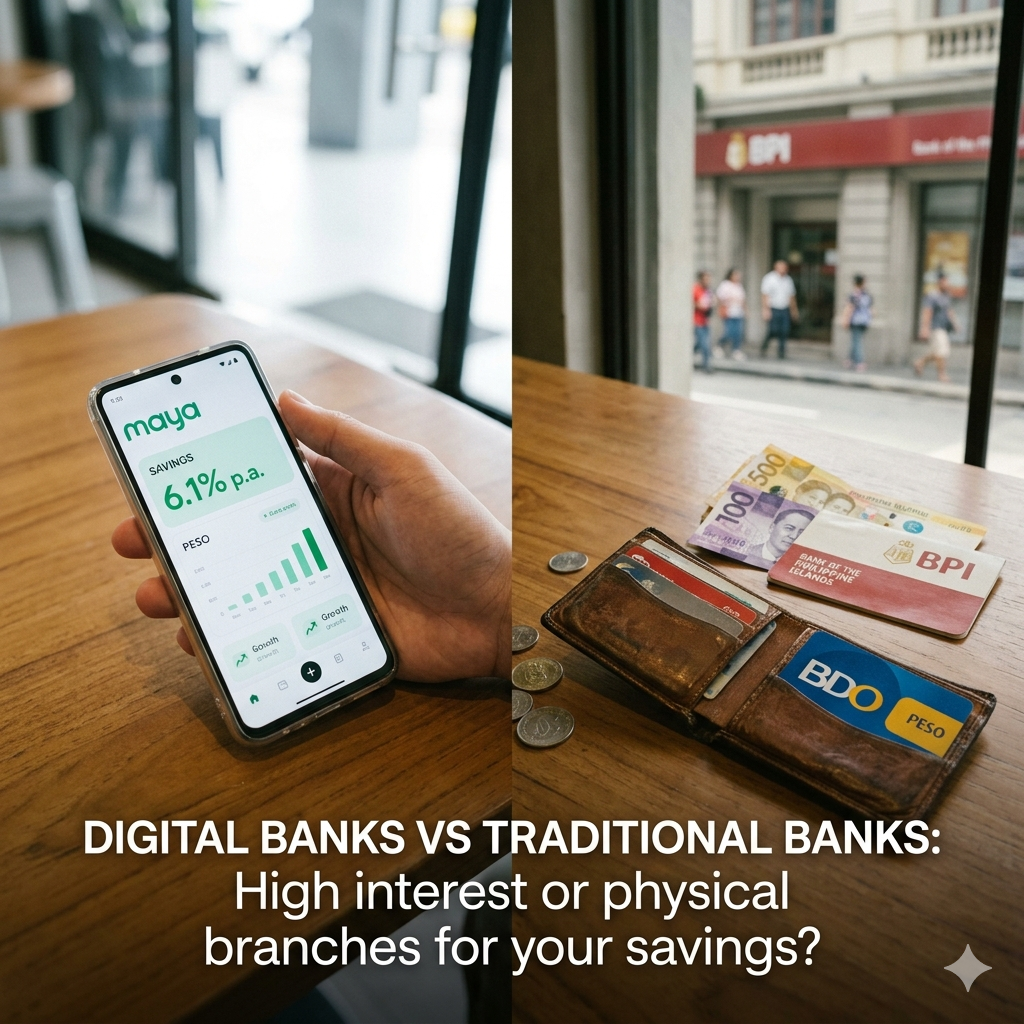

Digital banks update their rates constantly. Social media amplifies every change. And when you see that your current bank is paying 4% while another is advertising 7%, staying put feels like laziness.

Traditional banks still pay below 1% on regular savings accounts. Digital banks advertise 3% to 4% as a base, with promos pushing higher. That gap is real. Moving your money around feels like you're finally paying attention.

It feels like winning.

But winning at what, exactly?

The gap between a 4% and a 5% rate on ₱100,000 is about ₱1,000 a year. Less than ₱100 a month. And that assumes the higher rate stays, that you meet the conditions, and that none of your balance falls outside the cap.

The promise is big. The math is usually smaller.

Every transfer has a hidden tax. Not a fee. Something harder to measure.

Your time, attention, and mental energy.

Here's what actually happens when you move money between banks frequently:

Every move has a hidden stress fee. Even when it looks free.

👉 Are High-Interest Savings Accounts Too Good to Be True?

Ask yourself this honestly.

The last time something went wrong financially — a medical bill, an unexpected expense, a late payment — which account did you reach for first?

Not the one with the highest interest.

The one you trusted. The one you could access quickly. The one that worked when you needed it to.

That's the real job of a savings account.

Not to maximize yield on a spreadsheet. To be there when life doesn't go according to plan.

None of these things show up in a rate comparison table. But they're real. And they affect your life more than 1% ever will.

This is where most people overcomplicate things.

They try to find the one perfect account. The highest rate, the best app, the most accessible network, no maintaining balance, PDIC-insured, with goal-setting features and daily interest crediting.

That account doesn't exist. And trying to find it keeps you stuck in research mode forever.

The better move is to stop thinking about accounts as a single decision. Think about what your money actually needs to do.

Three buckets. Three different priorities. Three accounts that don't have to compete with each other.

Trying to optimize all three the same way is what creates the complexity.

Forget comparison articles for a moment. Ask yourself these instead.

The goal isn't the highest number. The goal is a setup that still works when things get stressful.

👉 The Difference Between Saving Money and Feeling Secure

Not all switching is bad. Some moves are worth making.

But switching because another bank is running a promo that's 0.5% higher? While you already have a decent, stable account that you trust?

That's not optimization. That's just restlessness.

Switch for real pain. Not for small bragging rights.

The saver who stays at a good-enough rate — consistently, without interruption, without splitting attention across five apps — usually ends up ahead of the saver who chases every new promo.

Here's why.

Ang saver na hindi naghahanap ng bago every month? Usually, they're the ones quietly winning.

Here's a simple checklist. If you can say yes to all four, your account is probably good enough — and your energy is better spent elsewhere.

If all four are yes, you're done. Stop looking.

Put that decision energy into earning more. Budgeting better. Or starting to invest — where the returns are much bigger than any savings rate difference ever will be.

The best savings account isn't the one with the most impressive number in a comparison table.

It's the one you trust when something goes wrong.

It's the one you don't have to think about every month.

It's the one that's still there, still working, still accessible — when you actually need it.

Rate-chasing rarely improves outcomes. But a stable, simple setup? That compounds quietly in the background, month after month, without asking anything from you.

Calm is a feature. Not a consolation prize.