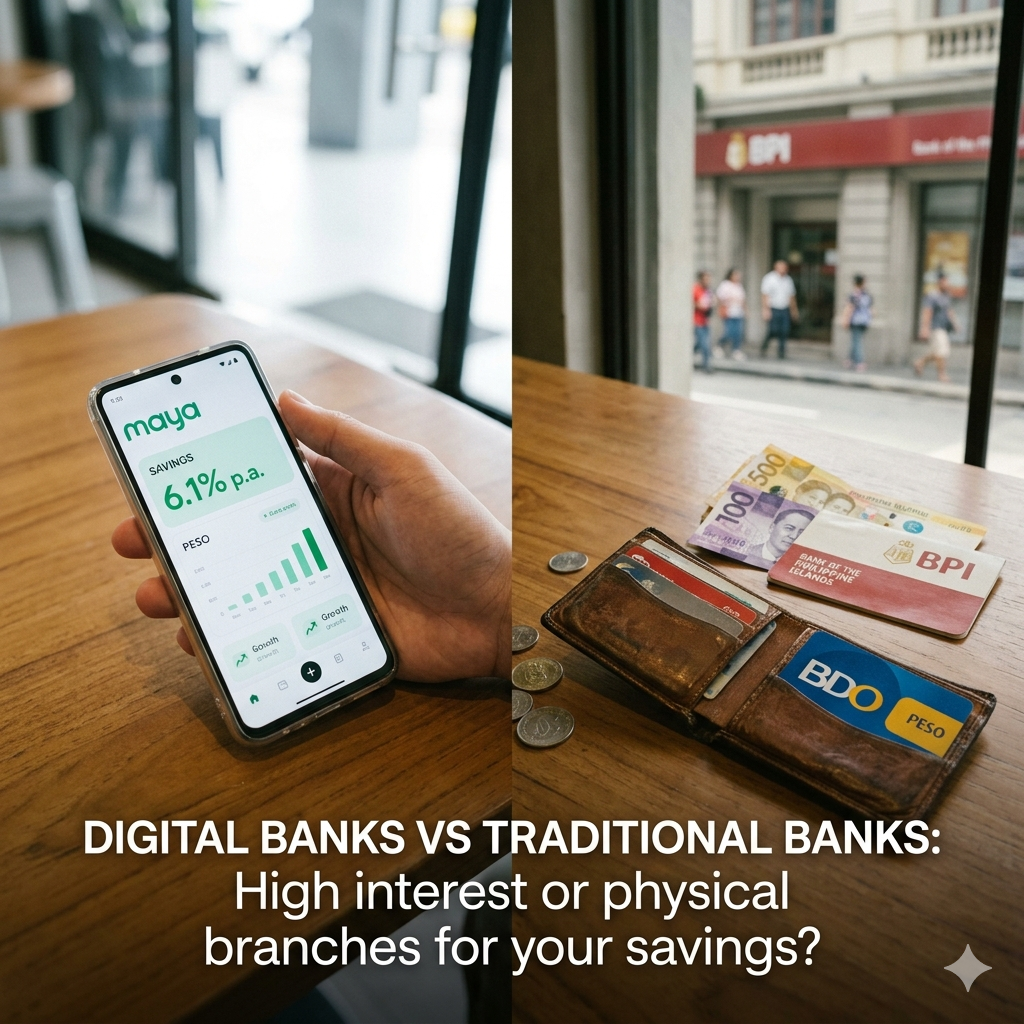

Digital Banks vs Traditional Banks for Savings

Choose where to keep savings based on your situation — not just headline rates.

You saw a savings account offering 10% interest. Maybe 12%. Maybe more.

And your first instinct was: may catch ba ito?

That instinct isn't wrong. But the answer is usually more boring than people expect.

High-interest savings accounts aren't scams. They're real products from real BSP-licensed banks, and they do pay out real interest.

But they come with conditions, caps, and expiry dates that a lot of people miss when they sign up. And those details change everything.

This article explains how these accounts actually work, why banks offer them, and how to tell if they're worth using for your situation.

If you're still figuring out where your savings should go in the first place, start here: 👉 Savings Account vs Time Deposit: What's Better for Filipinos?

It's not generosity.

Digital banks don't have branches. No tellers, no ATM networks to maintain. That saves them a lot on overhead, and part of those savings get passed on as higher interest rates to attract depositors.

But there's a more direct reason: competition.

The Philippine digital banking space is crowded. Maraming banks, same pool of savers. A high advertised rate is one of the fastest ways to get someone to open an account.

Think of it this way. Yung mataas na rate is their marketing spend. It's the cost of acquiring you as a customer. The hope is that once you're in, you'll use their card, pay bills through their app, maybe take out a loan down the line. That's where they actually make money.

The high rate is the hook. The ecosystem is the plan.

That's not inherently bad. You can absolutely benefit from the hook. But you need to understand what you're walking into.

This is where the disappointment usually starts.

Take Pau. He opened a digital savings account because of the advertised 10% interest. Masaya siya. He moved his savings in and waited for it to grow.

A few months later, he checked his earned interest.

Not 10%. Not even 8%.

3.5%.

The bank didn't cheat him. They paid exactly what was promised, based on the conditions he actually met. But Pau wasn't using their card. He wasn't paying bills through the app. He wasn't hitting the monthly spending targets.

So his rate quietly dropped to the base. Walang notification. Walang reminder.

This is how most high-interest accounts work:

Here's another common story.

Cel deposited ₱500,000 into a savings account advertising 10% interest. She didn't read the fine print closely. The app looked great, the rate looked great, so she assumed everything was fine.

At the end of the year, she did the math.

Turns out the 10% only applied to her first ₱100,000. Her remaining ₱400,000 earned 3.5%. Her actual blended rate for the year? About 4.6%.

Hindi masama — but very far from 10%.

This is the difference between two numbers that don't get talked about enough:

For most savers, the effective rate ends up significantly lower than the advertised one. Not because the bank is dishonest. But because:

Yung effective rate — that's the real number worth thinking about. Not the one on the poster.

There's one more thing that isn't always obvious: many of these high rates have an expiry.

"Up to X% until December 31." "Promo rate, subject to change." "Limited time offer."

It's written in the terms and conditions, pero hindi palaging naka-highlight sa ads.

What makes this frustrating is the timing. You made a decision based on that rate. You planned your savings around it. Then one day, the rate quietly changes. There's no drama, just a notification buried in the app that interest rates have been updated.

And suddenly you're earning the base rate again.

Situation: Enzo did this. He moved his emergency fund into a high-interest account because of an advertised 12% promo. His logic made sense: if the money is just sitting there, it might as well grow. Six months later, the promo ended. Rate dropped to 4%. He wasn't devastated, but he wished he hadn't moved his emergency fund there in the first place.

Treat promos as a bonus for a season. Not a plan for the next decade.

👉 Digital Banks vs Traditional Banks for Savings — why chasing the highest rate often backfires.

Usually, no. But there's a specific kind of risk worth naming.

If the bank is BSP-licensed and PDIC-insured, your deposits are protected up to ₱1,000,000 per depositor, per bank. That applies to digital banks the same way it applies to traditional ones. A high interest rate doesn't remove that protection.

The real danger isn't "this bank will disappear with my money."

The real danger is expectations.

When you make big financial decisions based on a rate that was never meant to be permanent — how large your emergency fund should be, when to start investing, how much house you can afford — that's where things go wrong.

The question to ask yourself isn't "is this bank safe?" It's: "am I making long-term plans around a short-term number?"

They work well in the right situations.

👉 Why Your Savings Keep Getting Used (And How to Fix It)

Not everyone should be chasing the highest rate. And that's completely fine.

Donna tried a high-interest account for a year. Every month, she had a mental checklist: spending missions, bill payments, balance levels. Her money was technically working harder. But she was also constantly second-guessing herself. Did she hit the requirement? Was she sure? How much did she actually earn this month?

After twelve months, she switched to a simpler digital savings account. Flat rate, no missions, no conditions. She earned slightly less on paper. But she stopped worrying about it entirely.

That peace of mind doesn't show up in any comparison table. But it's real.

Simple accounts have their own advantages:

Higher interest doesn't always mean higher peace of mind.

👉 The Difference Between Saving Money and Feeling Secure

You don't need to panic about the fine print. But five minutes of honest thinking before signing up is worth it.

If the answer to that last question is uncertain, a simpler account with a flat rate is probably a better fit.

A high interest rate is a nice feature. It isn't a financial plan.

Use these accounts intentionally: for the right kind of money, for the right length of time, with a clear understanding of the conditions. Don't put your emergency fund there. Don't build big decisions around a rate that might change next quarter.

When it works, it works well. When it's treated like a promise instead of a tool, that's when people end up frustrated.

Use it like a bonus. Sleep better because of it, not despite it.