Credit Card Travel Rewards in the Philippines

New to travel rewards? This beginner-friendly guide explains how credit card travel points actually work in the Philippines.

Mia had been planning her Osaka trip for months. In her head, at least.

The actual booking? That happened in forty-five panicked minutes on a Tuesday night.

Her friend messaged saying fares were going up. She opened her bank app, saw her points balance, thought "sige na" and started converting to Mabuhay Miles without checking award availability first. By the time she found seats, the dates were slightly off from what she wanted. She booked anyway because she was already in the middle of it and the momentum felt hard to stop.

The trip was fine. But the routing was inconvenient. The fees were higher than she expected. And for weeks afterward she kept thinking she should have waited.

This is how most bad travel rewards decisions happen. Decisions made under pressure, when dates are fixed, prices feel urgent, and stopping feels harder than continuing.

The fix isn't more knowledge. It's doing the thinking before the pressure arrives.

That's what this check-up is for.

👉 Credit Card Travel Rewards in the Philippines

A quarterly check-up is not about optimising every point you have. It's about making sure that when a trip comes up, you already know where you stand.

You know your balance. You know when things expire. You've already thought loosely about whether a redemption makes sense. So when your friend messages you about fares going up on a Tuesday night, you're not making decisions from scratch under pressure. You're just confirming something you've already thought through.

That gap between "panicked first-time decision" and "calm confirmation of something already considered" is where most redemption regret lives. The check-up closes it.

Quarterly is the right frequency. Monthly is too often and it turns rewards into a hobby you didn't sign up for. Annual is fine for very casual travelers but too infrequent if you travel twice a year and points have expiry windows. Four times a year is enough to stay aware without staying obsessed.

Start here every time. It sounds obvious, but a lot of people genuinely don't know what they have.

Check your bank rewards balance — the points sitting in your BPI, Metrobank, RCBC, or whichever card you use. Check your airline miles balance if you have one — Mabuhay Miles, GetGo, KrisFlyer, wherever you've accumulated. Write it down somewhere, even just in your Notes app.

Then check expiry. When do your bank points expire? When was the last time you had activity on your Mabuhay Miles account? Mabuhay Miles needs at least one earn or redeem activity every two years to stay active — a fact that surprises a lot of people when they find out the hard way.

Research on Filipino loyalty programme users consistently shows that many people forget they even have points until an expiry notification appears. By then it's either too late or the urgency forces a bad decision. The check-up means you know before the notification comes.

The goal of this step is just a clear picture. How much do you have, where is it, and is any of it at risk of expiring before your next check-up?

This step is specifically about avoiding emotional attachment before you know the numbers.

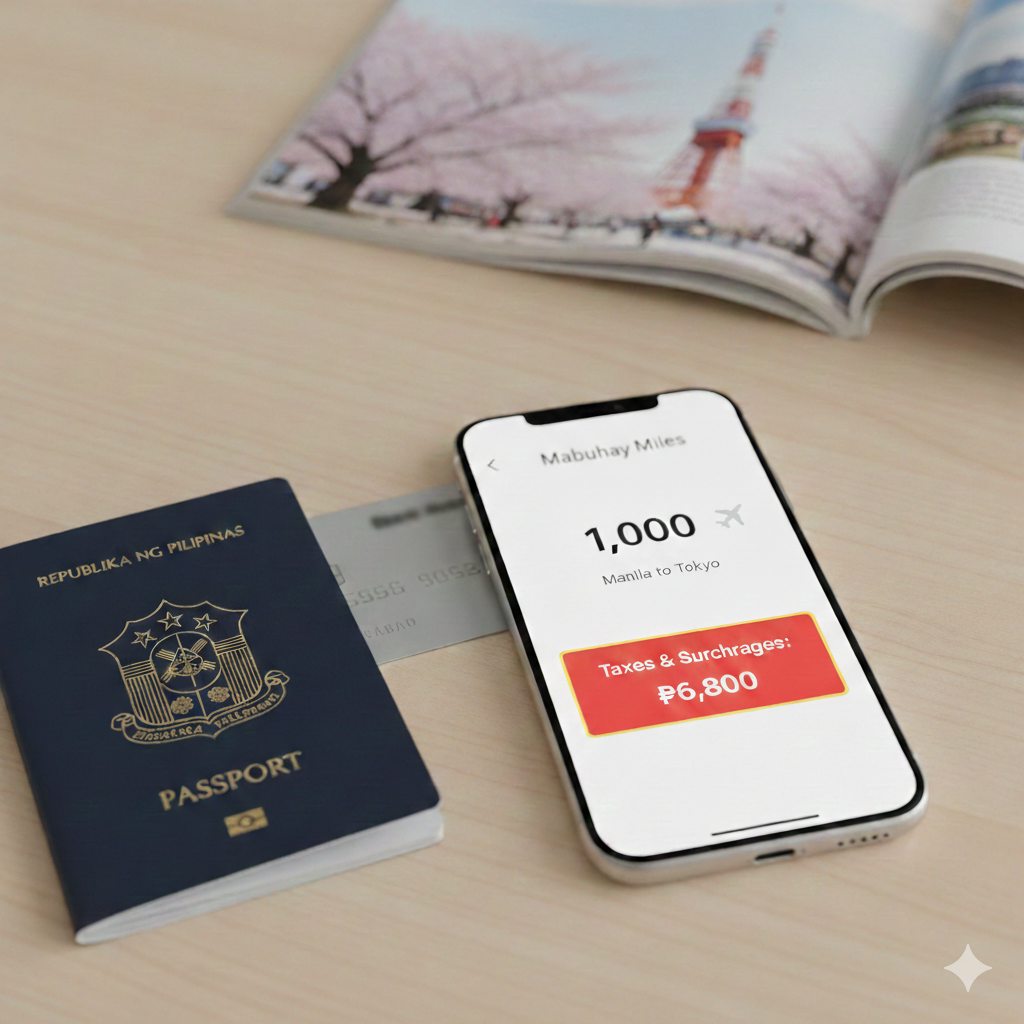

If you have a trip coming up in the next few months, search award availability on your target dates before you get excited about using points. Check what the total out-of-pocket cost would be — not just the miles required, but the taxes, fuel surcharges, terminal fees, and booking fees on top. For PAL Mabuhay Miles redemptions, these can be significant. A Manila to Incheon award ticket can still cost over ₱5,000 in fees even when the base fare is covered by miles.

Then compare that total to the current cash fare for the same flight.

This is the check people skip when they're making decisions under pressure. They see "award availability" and get excited and book before they've done the math. Then the confirmation page shows the fees and the excitement turns into that familiar "ah, ganito pala" feeling.

Doing this step during a calm quarterly review — not at 11pm while your friend is messaging you about fares — means you're comparing numbers without emotion clouding the picture.

👉 How to Redeem Airline Miles Without Wasting Them

Once you have the miles-plus-fees number and the cash fare number, ask the honest question.

Is using points actually better here?

Sometimes it clearly is. Long-haul flights during peak season, routes where cash fares are genuinely expensive — these are the moments where miles do meaningful work and the answer is obviously yes.

Sometimes it isn't. If there's a promo fare and the cash price is already low, the math on miles often collapses. You're replacing a small cash cost with a points redemption that still has fees attached, and the savings aren't significant enough to justify locking in award availability restrictions.

And sometimes it's genuinely close, which is useful information too. Close usually means either option is fine. Pick whichever is simpler.

The point of this step is to make the comparison calmly, before a trip is imminent. Not to always choose cash, not to always choose points, but to actually know which one makes more sense for this specific situation.

👉 Cashback vs Miles: Which Is Better for Filipino Travelers?

This step is easy to forget once you've had a card for a year or two. The annual fee becomes invisible — it gets charged, you accept it, you move on.

But it's real money, and it's part of the true cost of your rewards.

Most Philippine travel cards with meaningful miles earning charge annual fees between ₱4,000 and ₱6,000, sometimes waived in the first year and charged from the second onwards. If you earned back ₱3,000 in effective rewards value last year and paid a ₱5,000 annual fee, you're not ahead. You're down ₱2,000.

During your quarterly check-up, ask: based on what I've earned so far this year, am I on track to get more value out of this card than I'm paying in fees? If the answer is no, and it's been no for a while, that's worth paying attention to.

The other sign to watch for: are you making decisions specifically to justify the card? Booking trips you don't really need, forcing redemptions that don't quite work, keeping a card you barely use because it feels wasteful to cancel? That pressure is a signal. It means the card is working for the bank more than it's working for you.

👉 Annual Fees on Travel Cards: When Are They Actually Worth Paying?

This step sounds soft. It's actually one of the most useful.

Before you make any redemption decision, notice how you feel about it. Not what you think — how you feel.

Are you calm and clear about the numbers? Good. Are you feeling rushed, slightly anxious, or like you need to make a decision right now before something expires or a price goes up? That's a warning sign.

Urgency is the enemy of good travel rewards decisions. The feeling that you have to act now — before availability disappears, before the promo ends, before your points expire — is exactly the feeling that leads to the redemptions people regret. It bypasses the part of your brain that would normally compare options, do the math, and decide calmly.

Filipino consumer research shows that rewards programmes are specifically designed to create this kind of emotional pull. The expiry dates, the limited-time bonuses, the "only a few award seats left" warnings — these are not accidents. They're features. They work.

The check-up is your defence against them. By the time a sense of urgency appears, you've already done the thinking. You already know your balance, your options, and your rough sense of what's worth it. The urgency has less to grab onto.

If you sit down to do this step and realise you're already feeling stressed about your points, that's useful information. Stress is telling you something about the system you've built. Maybe it's too complex. Maybe there's an expiry coming up you'd forgotten about. Maybe you've been chasing something that doesn't actually match your life. Either way, the feeling is worth listening to.

After the five steps above, you'll usually land in one of three places.

The first: redeem now. The math is clearly good, availability works for your plans, fees are reasonable, and you're calm about it. Go ahead.

The second: pay cash and save points. The redemption doesn't offer better value than just buying the ticket, or the cash fare is cheap enough that points aren't needed. Pay cash, keep your balance for a better opportunity later.

The third: wait. You don't have a specific trip in mind right now. Nothing is expiring imminently. No redemption is obviously right at the moment. That's fine. Close the app and come back in three months.

Waiting is underrated. Points sitting in your account are not failing you. They're available when you need them. Forcing a redemption just to feel like you did something with your balance is one of the most reliably regrettable moves in travel rewards.

The check-up makes "wait" easier because you know your balance is safe, your expiry isn't imminent, and you haven't missed anything important. Waiting from a position of clarity feels very different from waiting out of avoidance.

Pull it all together and a healthy quarterly check-up takes maybe thirty minutes.

You look at your balances. You check expiry dates. If a trip is coming up, you search availability and run the numbers before you get emotionally attached to a specific redemption. You compare against cash. You factor in annual fees. You notice how you feel.

Then you make a calm decision — redeem, pay cash, or wait — and you don't think about your points again for another three months.

No spreadsheet. No daily monitoring. No restructuring your spending around promos. Just four brief check-ins a year that keep you aware without keeping you preoccupied.

The sign that this is working isn't a maximised points balance or a particularly impressive redemption. It's that rewards feel easy. Decisions feel clear. And when a trip comes up, you already mostly know what you're going to do before the pressure to decide arrives.

If a redemption feels rushed, it's probably not the right one.

Not because rushed decisions are always wrong, but because the feeling of urgency usually means something important hasn't been thought through yet. The math hasn't been checked. The fees haven't been added up. The comparison against cash hasn't been made.

The quarterly check-up exists to make sure all of that is done before the urgency appears. So that when the moment comes, you're not deciding. You're just confirming.

Mia does a check-up now. Every three months, thirty minutes, same six questions. Last December she used points for a Bohol trip during the long weekend. She'd already checked availability two months earlier, already knew the fees, already compared it against the cash fare. When she finally booked, it took ten minutes and felt completely straightforward.

"Parang wala lang," she said. "Dati ang stressful-stressful pa."

That's the whole goal.