Why Your Savings Keep Getting Used (And How to Fix It)

Why your emergency fund keeps getting drained and how to rebuild without guilt.

Celeste is 27, a nurse. She has one savings account she's been building for three years.

Last April, her mom got hospitalized. She pulled from her savings to cover the bills. No hesitation, that's what it was there for.

But when she checked her balance the week after, something felt off.

Her travel fund. Her "future business" money. Her three years of effort.

It all looked the same in one number. And now that number was smaller.

She hadn't done anything wrong. But it felt like she had.

That feeling is the problem.

Technically, one savings account works. The math is the same whether your money is in one place or three.

But emotionally and behaviorally? Most people struggle when emergency money, long-term goals, and everyday guilt all live in the same account.

This article explains why separating your emergency fund from your long-term savings often makes saving easier, not harder.

👉 If your savings keep getting used for the wrong things, start here: Why Your Savings Keep Getting Used (And How to Fix It)

Here's what happens when everything lives together.

You save ₱3,000 this month. You feel good.

Then the ref breaks. Or someone in the family needs help. Or a bill comes out bigger than expected.

You withdraw ₱2,500.

And instead of thinking "okay, I used my emergency buffer for an emergency" — you think: sira na yung savings ko.

That guilt is what makes people stop saving altogether.

When there's no separation, every withdrawal feels like failure. Every dip into the account feels like going backwards. And when saving feels like something you can't get right, a lot of people quietly give up tracking.

This isn't a discipline problem. It's a design problem.

Separating your money by purpose does three things.

It clarifies what each peso is for.

When money has a label, it's easier to decide whether spending it is allowed or not. "Pang-emergency" means yes during a crisis. "Pang-future" means no for impulse purchases.

It reduces guilt.

Emergency spending stops feeling like you're destroying your goals. Because you're not. You're using money that was already set aside for exactly that.

It speeds up decisions.

When something unexpected happens, you don't need to calculate whether you "can afford" to use your savings. You already know which pot it comes from and why it exists.

This is the real value of separation. It's not better interest rates or more accounts. Instead, you get clarity.

This is the account you're allowed to touch.

Jeric is 29, an IT support. He spent two years feeling guilty every time he used his savings for emergencies — a dental procedure, a broken laptop for work, a month where his freelance income dropped.

He kept thinking he was failing at saving.

He wasn't. He just had no dedicated emergency fund. So every withdrawal felt like he was spending his future instead of using his buffer.

An emergency fund should feel:

If you hesitate to use your emergency fund during an actual emergency, it's not functioning as an emergency fund. It's just labeled differently.

The goal is three to six months' worth of essential expenses. But start with one month. That alone changes how protected you feel.

👉 Emergency Fund First or Investing First? (A Filipino Reality Check)

This is the account you're not allowed to touch — at least not easily.

The whole point of long-term savings is friction.

Not the bad kind. The helpful kind. The kind that makes you pause before withdrawing and ask: is this actually what this money is for?

When your long-term savings are mixed in with your emergency fund, that friction disappears. Everything is accessible. Everything feels fair game.

Separate it, and suddenly that money feels protected. It feels slower. It feels like it belongs to a future version of you.

That mental boundary is what keeps impulsive withdrawals from quietly eating your goals.

Your long-term savings could be for a trip. A business. A house down payment. An investment fund you're building toward. It doesn't matter what the goal is. What matters is that the money isn't easily confused with your emergency buffer.

For most young Filipinos, three is enough.

That's it.

You don't need five accounts and a system that takes an hour to manage. You don't need a separate account for every goal.

Emergency funds are now the top stated savings priority for many Filipinos, ahead of travel and home upgrades. But only about 2 in 10 actually have three months' worth built up. The fix isn't more complexity. It's clarity about what money is for.

Three containers — even if two of them live inside the same banking app — is enough structure to start seeing the difference.

There's no official rule here. But a common and practical setup looks like this.

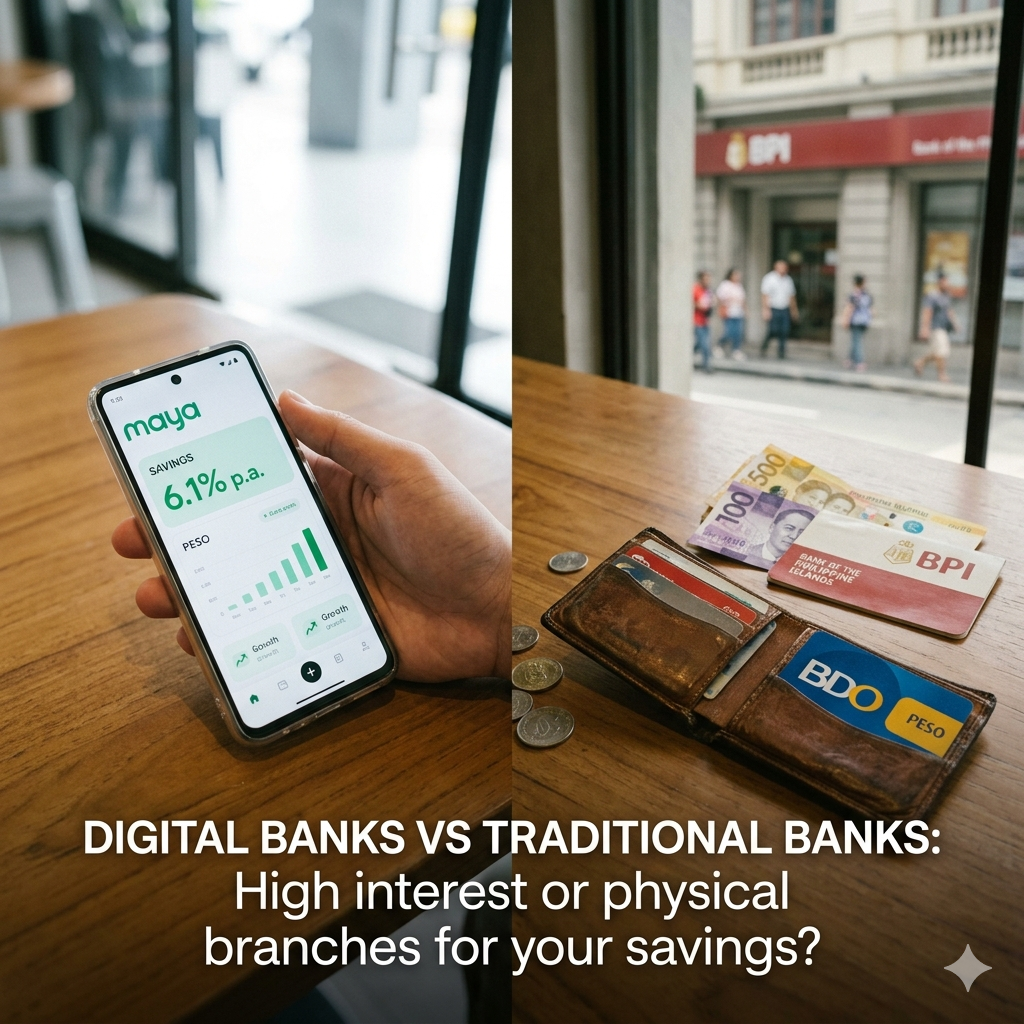

Traditional bank for emergency savings.

Familiar. ATM access. Payroll often goes here already. When something goes wrong at 10pm and you need cash fast, you know exactly where it is and how to get it.

Digital bank for longer-term savings.

Higher interest rates than most traditional savings accounts. Goal-tracking features. Sub-accounts or "pockets" that let you label and separate money within one app. Less tempting to touch because the UX is designed around saving, not spending.

This isn't the only setup. But it works because it uses each type of bank for what it's actually good at.

The key is access vs. separation. Emergency money should be easy to reach. Long-term money should feel a little harder to get to — not impossible, just not one-tap-away.

👉 Digital Banks vs Traditional Banks for Savings

There are situations where keeping things simple — meaning, one account — is the right call.

If your balance is very small.

If you're just starting and have less than ₱5,000 saved, splitting it into two accounts might make both feel too small to be meaningful. Focus on building the habit first. The structure can follow.

If you're overwhelmed.

Some people do better with one clear goal at a time. If opening a second account feels like too much to manage right now, that's valid. A simple setup you'll actually use beats a sophisticated one you'll abandon.

If you're still stabilizing income.

For freelancers, contractual workers, or anyone whose income is irregular, the first priority is just having something set aside, anywhere. The separation conversation comes after there's something to separate.

Start simple, then add structure later.

You don't have to move everything at once.

Start small:

Step 1. Open a second savings account. It doesn't need a big initial deposit. Some digital banks let you open with zero.

Step 2. Label one account "emergency" and one "goals." Even just the label changes how you think about the money.

Step 3. On your next sweldo, split your automatic transfer. Half to emergency, half to goals. Even if each amount is small, the habit of directing money with intention is what matters.

Step 4. Let it grow. You don't have to reorganize everything immediately. Just let separation happen naturally from this paycheck forward.

Mae is 24, a virtual assistant. She started with ₱500 in each account. Parang konti, she thought. But six months later, she had ₱4,000 in her emergency account and ₱3,500 building toward a trip to Siargao. Two clear pots. Two clear feelings.

She stopped feeling like her savings were one bad month away from disappearing.

👉 A Simple Savings System for Young Professionals

This isn't about control.

It's about clarity.

One account for everything works on paper. But in practice, mixed money creates mixed feelings. And mixed feelings make it harder to save consistently, spend without guilt, or use your emergency fund when you actually need it.

Separate the two, and everything gets a little easier.

Your emergency fund stops feeling like a rainy-day fund you're afraid to touch. Your long-term savings stop feeling vulnerable to every unexpected expense.

They each do their job. And you stop feeling like saving is something you can't get right.